Search posts

Stick to your values

Investing money can be an uncomfortable experience. For me, that discomfort occurs when I decide to challenge the market consensus and the prevailing investment wisdom. The easy option, of course, is to pay attention to the noise and follow the momentum. I deal with the discomfort by sticking to my values. What does this mean? For me, this means;

- Having a clear sense of what the current market is pricing in relative to my view on the fundamental outlook,

- Having a strong sense of where true valuations lie, even if markets are moving to the extreme and,

- Having a disciplined investment process that requires me to buy when markets are falling and sell when markets are rising.

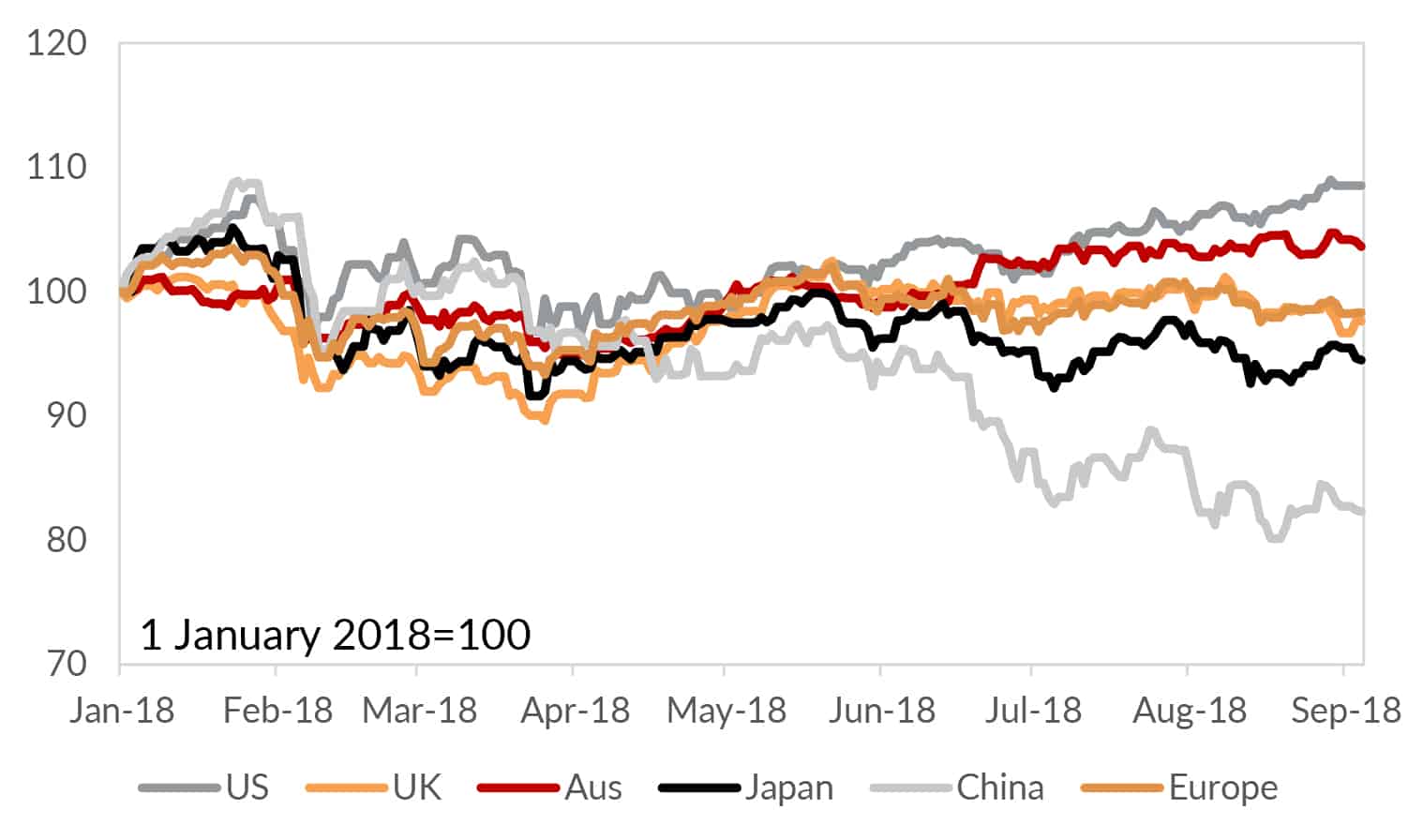

But in practice, how do I ensure I am being true to my values? I start with a belief that current asset prices convey information about the expectations of the market. Take equities, for example. The price of an equity index reflects the expected future cash flows (i.e earnings) of the underlying stocks in that index, discounted back to present value using an appropriate interest rate. I can use that information to estimate what the current price is telling me about the broader market’s expected future earnings. I can also use that information to estimate a fair value for an index. This process gives me clarity around the expected risk-adjusted returns over the near- to medium-term. I can perform similar experiments for each of the assets that sit in our portfolios. This gives me a clear thesis for each of the positions in the portfolio. I aim to allocate more to assets that have relatively higher risk-adjusted returns. And allocate less to assets that have relatively lower risk-adjusted returns. Let’s tie this in to what has been happening in markets. The US S&P500 has had strong recent relative performance versus other major indices (see Figure 1). Is this justified, or are we heading for a correction. And what can we do about it?

Figure 1: US equities have collectively outperformed over 2018

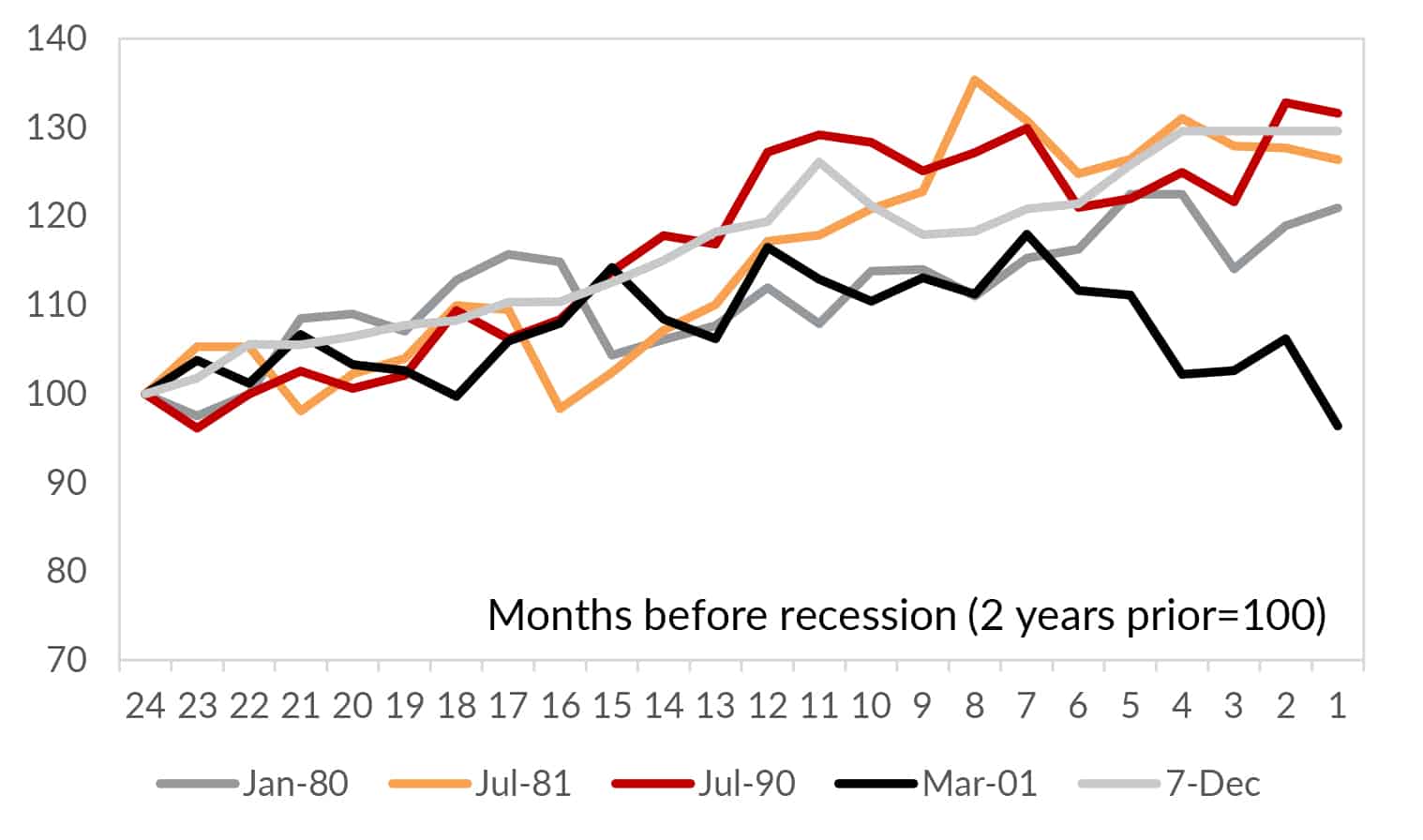

Right now, my quantitative assessment is that the US S&P500 is slightly above fair value. That fundamental view builds in my outlook that the US is headed for recession by 2021. If I think that the S&P500 is slightly above fair value, why am I invested? The answer is linked closely to how US equity markets have historically acted in the lead up to recessions. I call this period “late-cycle”. Late-cycle dynamics typically include a surge in merger and acquisition activity and share buy-backs. This pushes the equity market further above fair value prior to recession, offering reasonable risk-adjusted returns (Figure 2).

Right now, my quantitative assessment is that the US S&P500 is slightly above fair value. That fundamental view builds in my outlook that the US is headed for recession by 2021. If I think that the S&P500 is slightly above fair value, why am I invested? The answer is linked closely to how US equity markets have historically acted in the lead up to recessions. I call this period “late-cycle”. Late-cycle dynamics typically include a surge in merger and acquisition activity and share buy-backs. This pushes the equity market further above fair value prior to recession, offering reasonable risk-adjusted returns (Figure 2).

Figure 2: US equity markets have typically rallied during late-cycle periods

The equity portion of our portfolios currently overweight US, Japanese and Asia (including China) equites, and underweights European, UK and non-Asia EM equities. These positions are based on our assessment of the relative risk-adjusted returns on offer over the near and medium term. What are the risks to these positions? The major one is that a recession will unwind many of the gains when the market moves to fully price the impact of recession. How do I deal with that risk? After all, it is now the second longest economic expansion, and the longest equity bull market run, on record in the US. The probability of recession over the next five years is high. There are three important aspects of the investment process that help:

The equity portion of our portfolios currently overweight US, Japanese and Asia (including China) equites, and underweights European, UK and non-Asia EM equities. These positions are based on our assessment of the relative risk-adjusted returns on offer over the near and medium term. What are the risks to these positions? The major one is that a recession will unwind many of the gains when the market moves to fully price the impact of recession. How do I deal with that risk? After all, it is now the second longest economic expansion, and the longest equity bull market run, on record in the US. The probability of recession over the next five years is high. There are three important aspects of the investment process that help:

- A crucial part of our investment process is rebalancing away from markets that have outperformed to markets that have underperformed. This forces the portfolio to sell when prices have increased and buy when prices have decreased.

- I regularly update our assessment of fair value. I want to know when fundamental valuations have stretched so far that risk-adjusted returns look weak over the medium term. This is part of the dynamic asset allocation process.

- I spend a lot of time ensuring the portfolios are appropriately diversified. This includes having appropriately sized allocations to assets that may perform well if recession occurs sooner than expected – for example, high quality government bonds.

Importantly, it also includes allocating to alternative assets that are less correlated to the global macroeconomic environment. Building a well-diversified portfolio remains one of the best ways to protect against downside. If you want further clarity about how we can help you stick to your values, or are worried about how your portfolio might perform during an economic correction, please get in touch with us here to discuss how our resilient portfolio management can help.

This presentation material and all the information contained herein is the property of Oreana Financial Services Limited (OFS), and is protected from unauthorized copying and dissemination by copyright laws with all rights reserved. This presentation material, original or copy, is reserved for use by authorized personnel within OFS only and is strictly prohibited from public use and/or circulation. OFS disclaims any responsibility from any consequences arising from the unauthorized use and/or circulation of this presentation material by any party. This presentation material is intended to provide general information on the background and services OFS. No information within this presentation material constitutes a solicitation or an offer to purchase or sell any securities or investment advice of any kind. The analytical information within this presentation material is obtained from sources believed to be reliable. With respect to the information concerning investment referenced in this presentation material, certain assumptions may have been made by the sources quoted in compiling such information and changes in such assumptions may have a material impact on the information presented in this presentation material. In providing this presentation material, OFS makes no (i) express warranties concerning this presentation material; (ii) implied warranties concerning this presentation material (including, without limitation, warranties of merchantability, accuracy, or fitness for a particular purpose); (iii) express or implied warranty concerning the completeness or relevancy of this presentation material and the information contained herein. Past performance of the investment referenced in this presentation material is not necessarily indicative of future performance. Investment involves risks. Investors should refer to the Risk Disclosure Statements & Terms and Conditions of the relevant document for further details. This material has not been reviewed by the Securities and Futures Commission of Hong Kong.

Related Posts

Insights

Read our latest insights to help you make better investment decisions and build stronger portfolios.

Melbourne

Level 17, 627 Chapel Street, South Yarra, Melbourne, Victoria, 3141

Australia

T +61 3 9804 7113

F +61 3 9804 8377

Please email your request to

info@oreanafinancial.com

Sydney

Level 3, 31 Alfred Street,

Sydney, NSW 2000

Australia

T +61 3 9804 7113

F +61 3 9804 8377

Please email your request to

info@oreanafinancial.com

Hong Kong

Suite 1002, 10th Floor

Cambridge House, Taikoo Place

979 King’s Road, Quarry Bay, Hong Kong

T +852 3185 0200

F +852 2110 0736

Please email your request to

info@oreanafinancial.com

A Licensed Financial Firm

In Hong Kong we are licensed by the Securities and Futures Commission (license no. AHX191), the Insurance Authority (license no. FB1443) and the Mandatory Provident Fund Authority (license no. IC000563).

In Australia we are licensed by the Australian Securities and Investments Commission (AFSL No: 482234, ABN 91 607 515 122).