Search posts

This time isn’t different

The US yield curve inverted in early December. An inverted yield curve has been a very clear leading indicator for US recession over the many decades. We should start preparing for this outcome. But will the signal continue with its impressive track record? Or is this time different?

Early warnings

The spread between the 5-year and the 2-year US Treasury Bond yield turned negative (i.e inverted) in early December (see Figure 1). This spread is typically upward sloping. Longer-dated bonds normally have higher yields reflecting the risk premium associated with longer maturities. We view the spread between the 10-year Treasury yield and the 2-year Treasury yield as the most reliable indicator of US recession. This spread has not yet inverted. But we expect it will follow the shorter-dated spread in coming months. It always has in the past.

Figure 1: The yield curve has inverted

We are late cycle, headed for recession

An inverted curve supports our thesis that we are in the late economic cycle. Recession will follow. But it is important to note that curve inversion is a leading indicator. If history is anything to go by, we could be 18 to 24 months from recession. We have been anticipating a recession in end-2020 for some time. An inverted curve is a signal for recession but also a driver. US banks make money by borrowing short dated funds and lending longer dated funds. The inverted curve will impact profitability. Credit conditions will be tightened. We expect further liquidity tightening will be difficult for indebted balance sheets in the US. This will lead to increasing defaults particularly in the riskier parts of the credit spectrum. And rising defaults will give way to recession.

Now is the time to prepare, not to panic

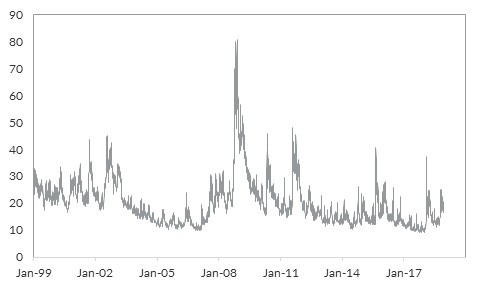

The yield curve is now likely to remain flat and bump around zero for some time. This flat period tends to last until the US Federal Reserve starts cutting the Fed Funds rate. This takes place when recession hits – so we have roughly two years of flatness. On average, the flat period has coincided with average S&P500 returns of around 20% over 18 months. That 18 month ride has historically been a bumpy one. We expect this time will not be different. We have already seen a shift higher in S&P500 volatility (Figure 2). We think this will persist. Still, it is not time to completely disengage from equity risk. We expect returns will remain moderately positive over the next 18 months. But reducing exposure given the higher risk may be appropriate.

Figure 2: Equity volatility is on the rise

Diversity can help

We’ve talked often about improving diversity within portfolios to protect against downside risks. Table 1 shows even this has been challenging in 2018. In the year to end-November, an investor with a simple allocation of 60% in global equities and 40% in global investment grade fixed income would have experience a 3.1% loss. Adding alternatives can help. We define alternative investments as something other than a simple long-only position in either equities or fixed income. Alternatives are a broad asset class. We aim to select alternatives that provide downside protection and low volatility. This includes pricing arbitrage funds, alternative credit funds, global multi-asset and global macro funds, and long-short funds that can help protect against falling markets – by either generating positive returns or reducing portfolio volatility. We are less interested in high-risk alternatives that we think tend to increase exposure to global market risk. A 25% position in alternatives and scaling down equity and fixed income exposure to 50% and 25% reduces the portfolio loss to 2.8%.

Table 1: Market movements

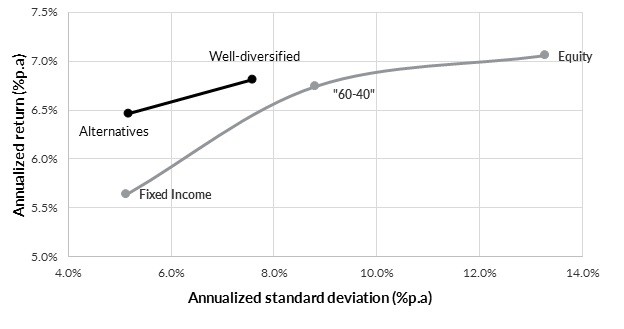

We have been adding alternatives to our portfolios through the year. Through the year, our Moderate Risk portfolios have outperformed their benchmark as a result by an average of 100bps. Over a longer period, since 1990, we have found that a well-diversified portfolio that includes equity, debt and alternatives has provided superior risk-adjusted returns to a less well-diversified portfolio (see Figure 3).

We have been adding alternatives to our portfolios through the year. Through the year, our Moderate Risk portfolios have outperformed their benchmark as a result by an average of 100bps. Over a longer period, since 1990, we have found that a well-diversified portfolio that includes equity, debt and alternatives has provided superior risk-adjusted returns to a less well-diversified portfolio (see Figure 3).

Figure 3: Well diversified portfolios including alternatives improve the risk-adjusted return opportunity

We have also built a portfolio of alternatives only. We call this our Diversified Alternatives portfolio. In October, a month where global equities were down 7.1%, our Diversified Alternatives Portfolio was up 0.18%.

We have also built a portfolio of alternatives only. We call this our Diversified Alternatives portfolio. In October, a month where global equities were down 7.1%, our Diversified Alternatives Portfolio was up 0.18%.

Summary

We expect a mildly positive outcome in US and global equities over the next 18 months. It is going to be an uncomfortable ride for investors that have become used to low volatility. Our response to this outlook has been to access alternatives and work the diversity within our portfolios. If you would like to learn more about how our broad range of portfolios or our Diversified Alternatives Portfolio can help you manage risk, visit our portfolio management service or directly get in contact with us here.

This presentation material and all the information contained herein is the property of Oreana Financial Services Limited (OFS), and is protected from unauthorised copying and dissemination by copyright laws with all rights reserved. This presentation material, original or copy, is reserved for use by authorised personnel within OFS only and is strictly prohibited from public use and/or circulation. OFS disclaims any responsibility from any consequences arising from the unauthorised use and/or circulation of this presentation material by any party. This presentation material is intended to provide general information on the background and services OFS. No information within this presentation material constitutes a solicitation or an offer to purchase or sell any securities or investment advice of any kind. The analytical information within this presentation material is obtained from sources believed to be reliable. With respect to the information concerning investment referenced in this presentation material, certain assumptions may have been made by the sources quoted in compiling such information and changes in such assumptions may have a material impact on the information presented in this presentation material. In providing this presentation material, OFS makes no (i) express warranties concerning this presentation material; (ii) implied warranties concerning this presentation material (including, without limitation, warranties of merchantability, accuracy, or fitness for a particular purpose); (iii) express or implied warranty concerning the completeness or relevancy of this presentation material and the information contained herein. Past performance of the investment referenced in this presentation material is not necessarily indicative of future performance. Investment involves risks. Investors should refer to the Risk Disclosure Statements & Terms and Conditions of the relevant document for further details. This material has not been reviewed by the Securities and Futures Commission of Hong Kong.

Related Posts

Insights

Read our latest insights to help you make better investment decisions and build stronger portfolios.

Melbourne

Level 17, 627 Chapel Street, South Yarra, Melbourne, Victoria, 3141

Australia

T +61 3 9804 7113

F +61 3 9804 8377

Please email your request to

info@oreanafinancial.com

Sydney

Level 3, 31 Alfred Street,

Sydney, NSW 2000

Australia

T +61 3 9804 7113

F +61 3 9804 8377

Please email your request to

info@oreanafinancial.com

Hong Kong

Suite 1002, 10th Floor

Cambridge House, Taikoo Place

979 King’s Road, Quarry Bay, Hong Kong

T +852 3185 0200

F +852 2110 0736

Please email your request to

info@oreanafinancial.com

A Licensed Financial Firm

In Hong Kong we are licensed by the Securities and Futures Commission (license no. AHX191), the Insurance Authority (license no. FB1443) and the Mandatory Provident Fund Authority (license no. IC000563).

In Australia we are licensed by the Australian Securities and Investments Commission (AFSL No: 482234, ABN 91 607 515 122).