Search posts

Climbing the wall of worry

Evergrande. The US debt ceiling. Federal Reserve QE tapering. Supply shortages. Oil prices. Stagflation. High valuations.

The list goes on. Global investors face a wall of worry that has many questioning the prospects for further equity market gains. Recent market volatility has been challenging. That has made it difficult to look through the headlines to the strong fundamentals beyond.

We expect global growth will remain solid in in the near-term. And that leaves us optimistic on equity market returns over the medium-term.

Low growth, high inflation? We don’t think so

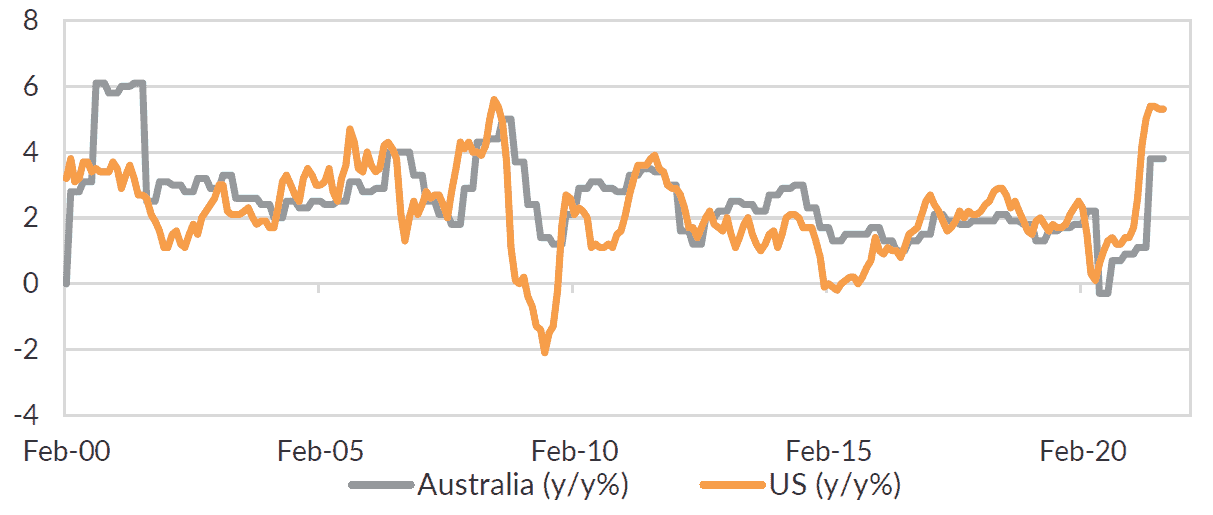

In many developed economies, inflation is above the central bank targets. Supply chain disruptions have pushed prices higher for many goods and services. Wage growth is normalising following the pandemic. Oil prices are almost 60% higher year-to-date.

Figure 1: Inflation is elevated in the US and Australia relative to recent history

Higher inflation will at least partially be transitory. Many of the impacts will begin to normalise over the coming 12 months. But some of it will be more persistent. We expect wages growth to revert to higher levels than immediately pre-pandemic. This will coincide with productivity increases. The outcome is wage growth that will benefit households without being overly inflationary.

At the same time, growth is slowing. Growth surged after Covid19-related lockdowns. The reopening pushed growth to unrealistically high levels from very low bases. The normalisation process is occurring now. We should expect growth to move back towards more historically normal levels through 2022 and 2023.

Higher bond yields, higher equities

The economic growth and inflationary outlook all but ensures that the US Federal Reserve will begin reducing its asset purchase program this year. Other central banks have already started tapering. And rate hikes are on the cards in some developed economies over the next three to four months.

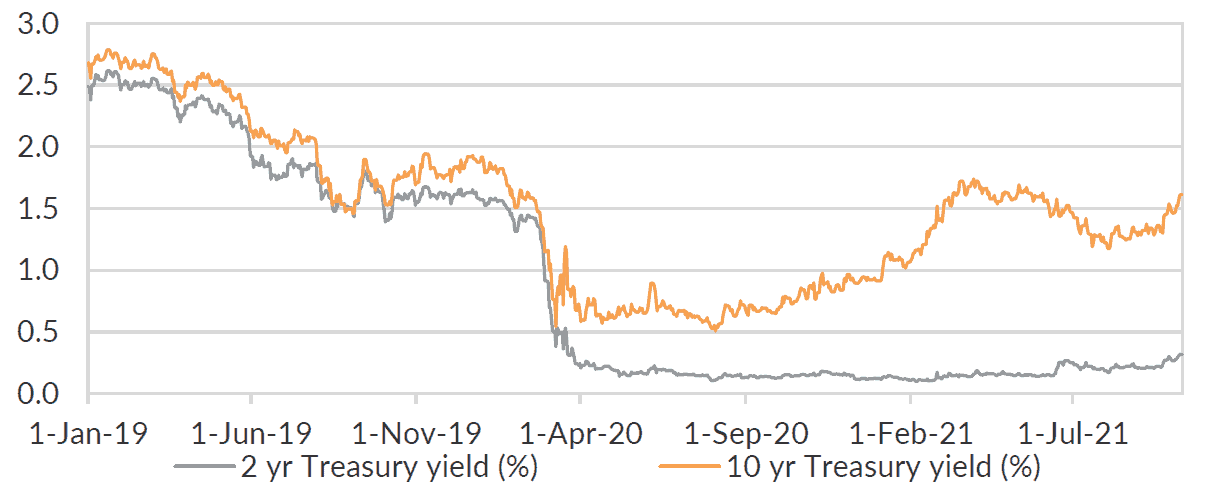

We expect that will lead to higher government bond yields. The US Treasury 10-year yield, for example, is currently around 1.6%. We have previously forecast that yield to rise to around 2% by end-2021 and to reach as high as 3% over the coming 18 months.

Figure 2: US Treasury yields have moved higher, and we expect have further to go

That doesn’t need to spell negative outcomes for global equities. Higher bond yields in this case reflects reasonable growth outcomes, inflation normalising to central bank targets, and central banks beginning to move policy rates higher gradually. This remains a positive environment for corporate revenues and earnings growth. We also expect that as rates do drift higher, many corporates will take the opportunity to issue debt and buyback equities, adding support to equities over the medium-term.

Stay invested

September was one of the worst months in recent years for a typical balanced portfolio. Equites and bond prices fell. Those types of market movements can prompt reactionary moves within portfolios. We recommend holding the course. In some markets, we suggest adding to risk. Despite the near-term volatility, we expect global equities to continue to climb a wall of worry and deliver strong medium-term risk adjusted returns.

Contact PAS for more information

The Portfolio Advisory Service has been working with clients across Australia and Asia to help manage investment solutions. Our work is supported by deep asset class research and manager review expertise within the team.

Reach out to our Portfolio Advisory Service to find out how we can assist you with managing your investment challenges.

This presentation material and all the information contained herein is the property of Oreana Financial Services Limited (OFS), and is protected from unauthorised copying and dissemination by copyright laws with all rights reserved. This presentation material, original or copy, is reserved for use by authorised personnel within OFS only and is strictly prohibited from public use and/or circulation. OFS disclaims any responsibility from any consequences arising from the unauthorised use and/or circulation of this presentation material by any party. This presentation material is intended to provide general information on the background and services OFS. No information within this presentation material constitutes a solicitation or an offer to purchase or sell any securities or investment advice of any kind. The analytical information within this presentation material is obtained from sources believed to be reliable. With respect to the information concerning investment referenced in this presentation material, certain assumptions may have been made by the sources quoted in compiling such information and changes in such assumptions may have a material impact on the information presented in this presentation material. In providing this presentation material, OFS makes no (i) express warranties concerning this presentation material; (ii) implied warranties concerning this presentation material (including, without limitation, warranties of merchantability, accuracy, or fitness for a particular purpose); (iii) express or implied warranty concerning the completeness or relevancy of this presentation material and the information contained herein. Past performance of the investment referenced in this presentation material is not necessarily indicative of future performance. Investment involves risks. Investors should refer to the Risk Disclosure Statements & Terms and Conditions of the relevant document for further details. This material has not been reviewed by the Securities and Futures Commission of Hong Kong.

Related Posts

Insights

Read our latest insights to help you make better investment decisions and build stronger portfolios.

Melbourne

Level 17, 627 Chapel Street, South Yarra, Melbourne, Victoria, 3141

Australia

T +61 3 9804 7113

F +61 3 9804 8377

Please email your request to

info@oreanafinancial.com

Sydney

Level 3, 31 Alfred Street,

Sydney, NSW 2000

Australia

T +61 3 9804 7113

F +61 3 9804 8377

Please email your request to

info@oreanafinancial.com

Hong Kong

Suite 1002, 10th Floor

Cambridge House, Taikoo Place

979 King’s Road, Quarry Bay, Hong Kong

T +852 3185 0200

F +852 2110 0736

Please email your request to

info@oreanafinancial.com

A Licensed Financial Firm

In Hong Kong we are licensed by the Securities and Futures Commission (license no. AHX191), the Insurance Authority (license no. FB1443) and the Mandatory Provident Fund Authority (license no. IC000563).

In Australia we are licensed by the Australian Securities and Investments Commission (AFSL No: 482234, ABN 91 607 515 122).